A news feature on the Atlas of Economic Complexity, the metric quietly underpinning every serious warning about Guyana’s oil-driven future.

When the World Bank’s April 2026 Latin America & Caribbean Economic Update warned that Guyana’s headline growth must be matched by broader-based, more inclusive development, it was drawing on a body of economic research that has been slowly transforming how growth itself is understood. At the centre of that research is a single, deceptively simple-looking dataset: the Atlas of Economic Complexity, run by the Growth Lab at Harvard’s Kennedy School of Government and led by Ricardo Hausmann, a former planning minister of Venezuela who has spent two decades arguing that what a country exports tells you almost everything about what it knows how to do and therefore about how rich it can credibly hope to become.

The Atlas was built around an index, the Economic Complexity Index, that Hausmann developed with César Hidalgo, then at the MIT Media Lab. The pair first set out the idea in a paper in the Proceedings of the National Academy of Sciences in 2009, and the project has since grown into one of the most-cited tools in development economics, used by governments, the World Bank, and investors trying to assess where countries are likely to go next. The latest version, Atlas 10.0, was released by the Growth Lab in September 2024, with rankings updated through 2022 trade data and the companion Observatory of Economic Complexity carrying numbers through 2024. None of it puts Guyana in a flattering light.

The argument behind the index is intuitive once you accept its premise. Hausmann and Hidalgo treat an economy not as a collection of factories and resources but as a pool of productive knowledge; the diffuse, hard-to-replicate, often unwritten know-how that lives in workers, firms, supply chains, regulators, and universities. Knowledge of that kind cannot be observed directly, but it leaves a fingerprint in the products a country can sell competitively on world markets. A country that exports semiconductors, precision instruments, and aircraft components is signalling that, somewhere in its workforce and institutions, it has assembled the capabilities those products require. A country that exports only iron ore or crude oil is signalling something quite different. Economists writing about the Atlas often describe the index using a restaurant metaphor: rather than peering into the kitchens of every economy, the ECI compares menus on the assumption that the kitchen behind a sophisticated, varied menu must itself be deep and well-equipped.

Mechanically, the index does two things at once. It measures diversity; the number of distinct products a country exports competitively and ubiquity; how many other countries also export those same products. A high score requires both; a wide range of products, and at least some of those products being rare globally. Japan, Switzerland, Germany, South Korea, Singapore, and Taiwan dominate the top of the rankings precisely because they sell many things that few others can make. The United States sits at fourteenth, the United Kingdom at tenth, China at eighteenth. The countries that have climbed fastest in the past decade; Hong Kong, North Macedonia, Armenia, Cambodia, have done so by adding new, more sophisticated products to their export menus, not by selling more of what they already had.

The reason any of this matters for policy is that the index is not merely descriptive. Hausmann and Hidalgo argue, with a substantial body of statistical evidence behind them, that the ECI is a stronger predictor of future GDP-per-capita growth than traditional measures of governance, competitiveness, or human capital, and that it shows a strong negative correlation with income inequality. Countries that diversify into more complex products, in their model, tend to grow faster and distribute the gains more evenly. Countries that double down on a single, ubiquitous commodity tend to plateau, regardless of how much money flows in during the boom. The Atlas also publishes a companion measure, the Complexity Outlook Index, which estimates how many sophisticated products are within reach of a country’s existing capabilities; a kind of forward-looking score for how easy diversification would be if the country chose to pursue it.

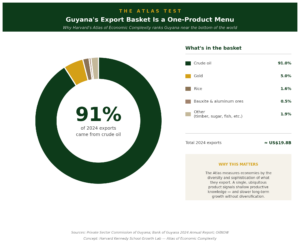

Against that framework, Guyana’s numbers are stark. According to the Private Sector Commission of Guyana, 91 percent of the country’s 2024 export earnings came from crude oil, on a total export figure of roughly US$19.8 billion. The Bank of Guyana’s 2024 Annual Report shows that everything else combined; gold, rice, bauxite, sugar, timber, fish, manufactured goods, and the long tail of smaller exports, totalled only about US$1.8 billion. The United Nations Economic Commission for Latin America and the Caribbean, working with slightly different definitions, put crude at 84 percent of Guyana’s export portfolio in mid-2024 and projected the country’s export value would grow by 77 percent that year, almost entirely on the back of higher oil volumes. Industry tracker OilNOW projected that crude would generate 89 percent of Guyana’s export value in 2025. By any of these slices, the export basket is now overwhelmingly one product, and that product is among the most ubiquitous and lowest-complexity goods on the Atlas’s product list, exported by dozens of countries and requiring almost none of the diffuse industrial knowledge the index is designed to capture. Guyanese economists writing in Stabroek News in late 2025 referenced this directly, placing the country in the bottom 10 percent globally on the Atlas’s diversification measures.

The implications run in three directions. The first is volatility: when one product is nearly all of your exports, a swing in its global price translates into an outsized swing in your fiscal revenues, foreign-exchange reserves, and current account, with limited ability to absorb the shock. The second is the so-called Dutch disease; the well-documented tendency of resource booms to push up the real exchange rate, raise the cost base for every other tradable industry, and crowd out the agriculture, light manufacturing, services, and tourism sectors that would otherwise diversify the economy. The IMF, in its May 2025 Article IV consultation with Guyana, explicitly flagged real exchange rate appreciation as a risk if domestic spending continued to outpace absorptive capacity.

The third, and longest-lasting, is what could be called the know-how trap: the deeper claim of the Atlas is that productive capability is built by making things, not by extracting them. A generation of young Guyanese growing up in an economy whose only large-scale industrial activity is offshore oil production may find, twenty years from now, that the country has the per-capita GDP of a wealthy nation but very little of the underlying productive infrastructure that would allow it to build the next industry once oil tapers.

It is fair to note the limits of the index. The Atlas measures exports rather than production, so it can undercount domestic-only activity in services, construction, and informal commerce. It does not account well for very small economies. And critics have long pointed to Norway as the case that complicates the story; Norway looks much richer than its complexity score predicts, because of an oil-management framework built around a sovereign wealth fund, strict fiscal rules, and decades of careful institutional investment that has insulated the rest of the economy from the resource boom. The Norwegian counter-example is not an argument against the Atlas; it is, if anything, an argument for why the institutional and investment-management cautions in the World Bank’s April 2026 report deserve to be taken with the seriousness Hausmann’s research suggests they merit.

Two booms are running through Guyana right now. One is the macro boom, captured neatly in the IMF’s growth tables and the World Bank’s projections. The other is the slower, deeper question the Atlas of Economic Complexity is built to answer; when this is over, what will Guyana have learned how to do? On present numbers, the answer is uncomfortable. But it is also, as the Atlas’s own architects argue, a question of policy choice rather than fate.